Competitive Procurement - Official Value Assessment

A Free, Independent ERCOT Procurement Assessment That Could Reveal Thousands in Annual Electricity Savings for Texas Commercial and Industrial Businesses.

Texas electricity markets are in a period of structural transformation.

ERCOT’s own adjusted forecast projects peak demand reaching 154 GW by 2035, nearly doubling from today. Transmission Service Provider (TSP) interconnection queue data suggests the number may be conservative, with some forecasts approaching 227 GW when large load interconnection requests are included.

Data centers alone account for the majority of incremental demand growth, scaling from roughly 3.7 GW of load in 2025 to a projected 86 GW by 2031 in the TSP queue model.

Against that backdrop, the question of whether commercial and industrial buyers should competitively procure their electricity supply, rather than remaining on default utility pricing or direct spot exposure, becomes worth examining carefully.

Not as a sales proposition but as a genuine market question.

The mechanics, plainly stated

Competitive procurement replaces a commercial buyer’s default energy supply arrangement, whether that’s a utility pass-through rate, an index-based contract, or unmanaged spot exposure, with a negotiated fixed or structured supply contract from a Retail Electric Provider. The buyer selects a term, a product type (fixed, indexed, hybrid, block-and-index), and a counterparty.

The REP prices the contract based on current forward curves, informed negotiation, embedded risk premiums, and their own cost-to-serve assumptions.

In ERCOT’s deregulated market, this process is entirely voluntary for commercial accounts above certain thresholds. The competitive market is real. The pricing signals are real.

The question is simply whether the mechanism delivers value, to whom, and under what conditions.

The value of procurement is not binary. It depends on when you do it, what you buy, and whether anyone in the transaction is working from complete information.

For more info;

The Bill Is Coming: Why Texas Business Owners Can No Longer Ignore the Power Market.

A structured assessment across five factors

Where the data is unambiguous

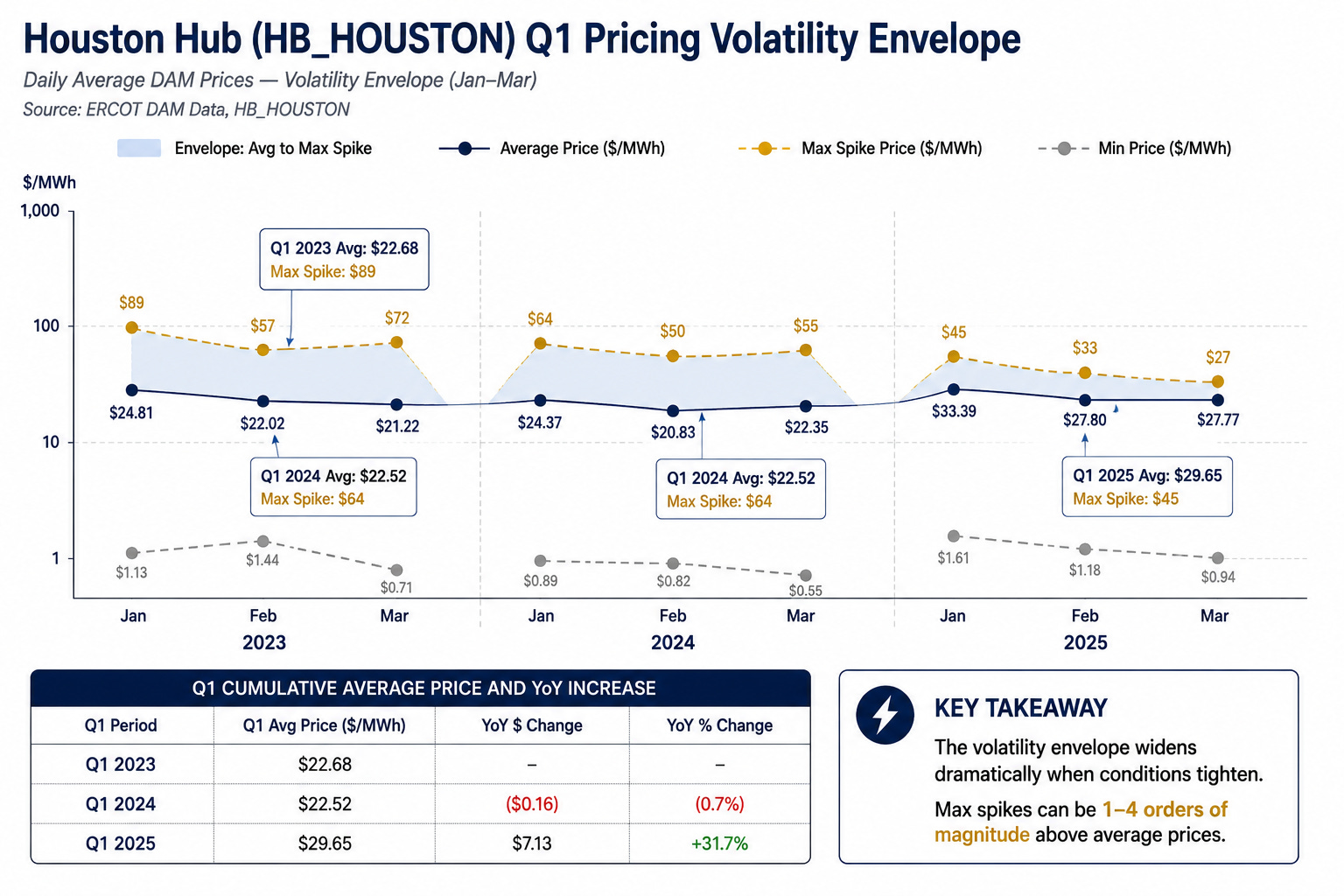

(Note: Q1 is the focal point due to its less volatile nature. You tend to see more raw structural volatility)

The volatility insulation argument is the strongest case for procurement in ERCOT, and the pricing data makes it concrete. HB_Houston’s, the hub capital of the US, maximum daily spike prices ran 1.5 to 4 times average prices within a single quarter across Q1 2023–2025.

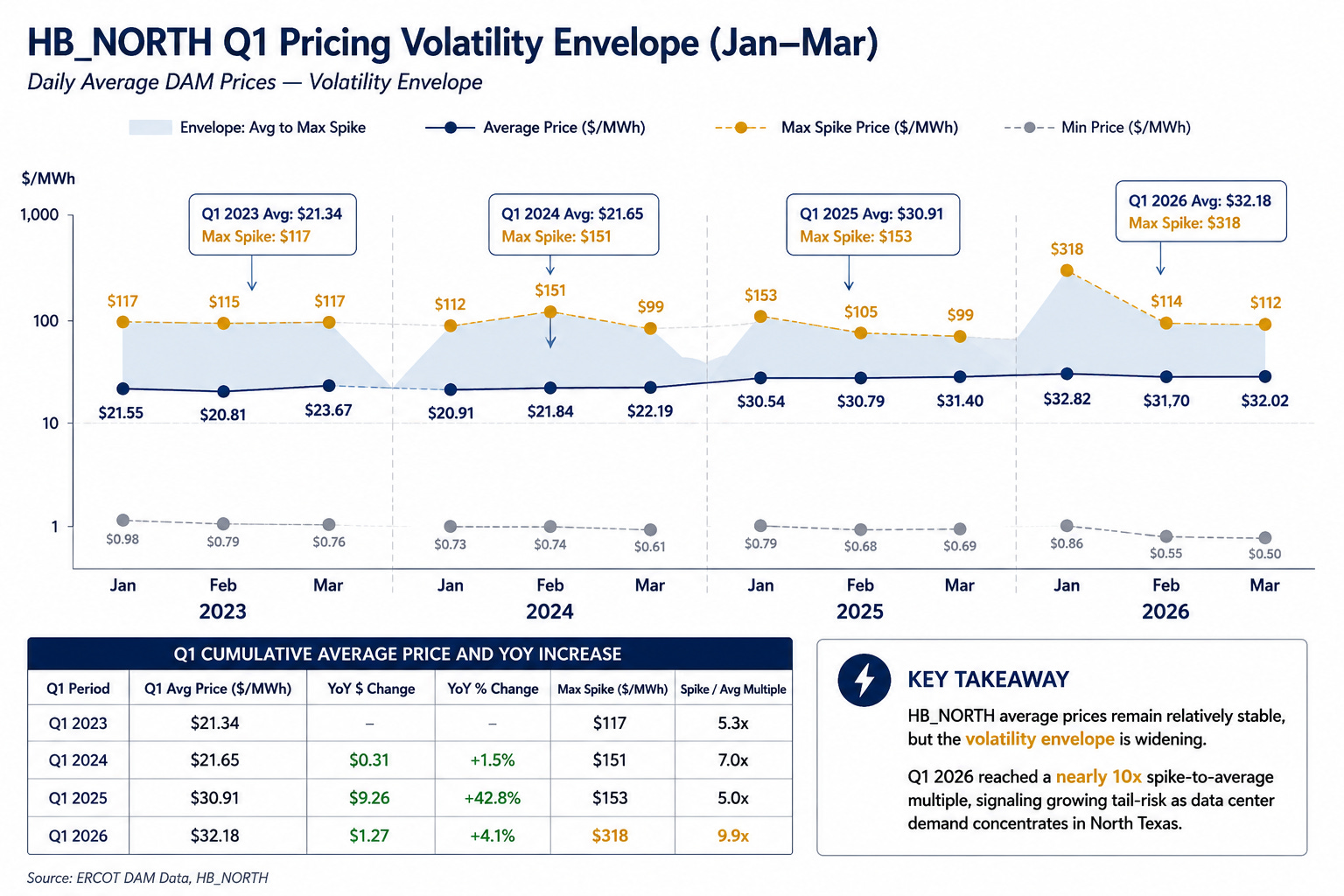

HB_North (DFW area hub) recorded a spike-to-average multiple of 9.9x in January 2026, a $318/MWh max against a $32.82 monthly average. These are not tail events in a statistical sense anymore. They are a structural feature of a grid absorbing load concentrations faster than transmission infrastructure can redistribute.

For commercial buyers with continuous, non-deferrable load; manufacturing operations, data center colocation, cold storage, hospitality, this volatility is pure cost variance with no upside.

A fixed supply contract converts that variance into a known, plannable number. Whether that number is “good” relative to what spot would have averaged over the contract term is a hindsight question. Whether it removes budget uncertainty is not.

The economic value of certainty is not equivalent to the economic value of a lower average cost.

For businesses with fixed revenue streams and tight operating margins, predictability has standalone value independent of whether the fixed rate outperforms spot in hindsight.

The two are often conflated in conversations about procurement, usually by parties with an interest in one framing over the other.

Free Savings Calculator | See How Much You Can Save

Where value is real but capture is incomplete

Forward curves already embed market expectations of future scarcity. When a buyer locks a three-year fixed rate in a structurally rising demand environment, they are not escaping that signal, they are buying a point on it. The question is whether they are buying it before or after the market has fully repriced the new demand regime.

The TSP load forecast data, showing data center load growing from 3.7 GW to 86 GW between 2025 and 2031, suggests that full repricing has not yet occurred in long-dated forward contracts.

The market digests this data gradually, through interconnection queue filings, ERCOT planning reports, and REP forward book updates. There is likely a window, though its duration is uncertain, in which forward curves still reflect partial rather than complete demand expectations.

The more persistent limitation is on the execution side. The standard channel through which most commercial buyers access competitive supply, retail brokers compensated by the REP on a per-kWh commission basis, creates an information asymmetry.

Commission structures of $0.002–$0.005/kWh embedded in contract pricing are not disclosed to buyers in most transactions. The incentive created by those structures points toward longer terms and higher-margin products, not necessarily the optimal outcome for the buyer’s load profile and risk tolerance.

The product exists. The market need is genuine. The gap between available value and captured value is almost entirely an information problem, not a market structure problem.

This does not mean procurement fails to deliver value through standard channels. It means a meaningful portion of available value is absorbed in the transaction rather than passed to the buyer.

How much depends on the specific REP, product, term, and market conditions at execution, none of which the buyer can independently evaluate without market data and an informed visibility.

What makes the current window different

The ERCOT grid has experienced demand growth before.

What is structurally different now is the nature and concentration of the incremental load.

Base residential and commercial load grew roughly 9% over the 2025–2031 forecast window in TSP data. With commercial electricity use will likely surpass residential in 2027: EIA

Data centers, crypto mining, industrial electrification, and hydrogen production account for the remaining growth, load categories that are price-insensitive, geographically concentrated, and highly continuous.

Price-insensitive load does not respond to high prices by curtailing. It bids for supply regardless of clearing price, compressing reserve margins and widening the volatility envelope for all remaining buyers. The HB_North spike multiplication, from 5.3x in 2023 to 9.9x in Q1 2026, is a direct readout of this dynamic.

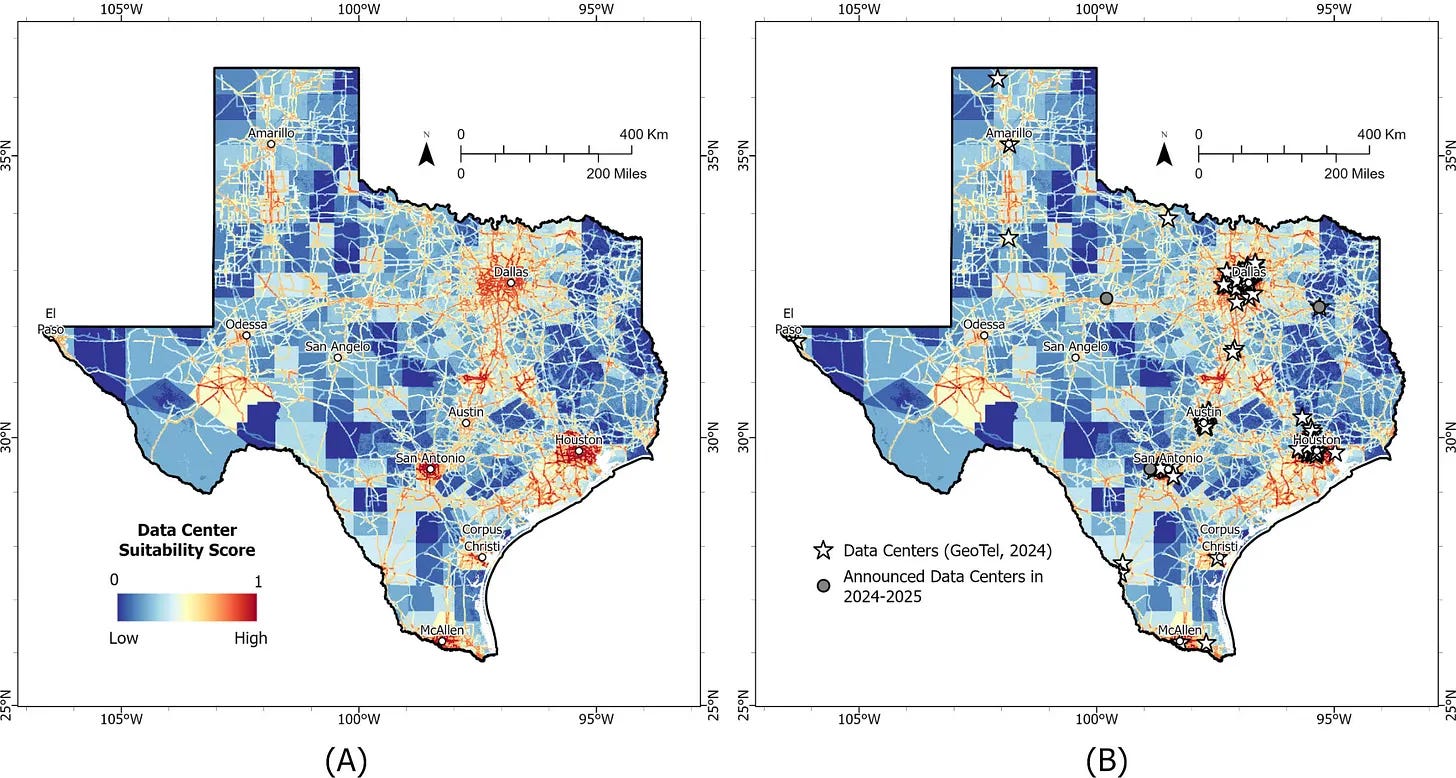

North Texas, where data center suitability scores and announced projects concentrate most heavily, is already showing the grid stress that the rest of ERCOT will experience over the next several years as load grows and geographic concentration increases.

On timing:

The question of whether to procure is separable from the question of when. In a structurally rising price environment, the timing decision carries real economic consequence.

Buyers who procured in 2022–2023, when HB_Houston averages were in the low $20s/MWh range, are sitting on favorable fixed rates relative to current market.

Buyers evaluating procurement today are pricing against a market that has already absorbed one significant repricing event (+31.7% YoY in Q1 2025) and has not yet fully priced the demand trajectory through 2031.

What the data supports, and what it doesn’t

Competitive procurement scores 7.3 out of 10 in our weighted assessment across the five dimensions most relevant to commercial buyers in ERCOT’s current market.

That is a genuinely high score and the grid data supports it: demand is growing non-linearly, volatility is structurally widening, and the geographic concentration of new load creates localized price stress that will propagate through the system over the next several years.

What the data does not support is the conclusion that procurement is uniformly valuable regardless of how it is executed. The single highest-leverage variable is the quality of information the buyer brings to the transaction.

A buyer who understands their load profile, current forward market conditions, embedded commission structures in REP offers, and the directional demand signal from ERCOT’s own planning data is in a fundamentally different position than one who is not.

The market exists. The value is real. Whether it reaches the buyer depends almost entirely on how the buyer approaches it.

Put It to the Test

Theory is useful. Your own electricity account is more useful.

We’re currently offering a limited number of complimentary Competitive Procurement Audits for Texas commercial and industrial businesses. We’ll review your current position, benchmark it against today’s market, and provide an objective assessment of where opportunities, or risks may exist.

If there’s value to uncover, we’ll show you. If there isn’t, we’ll tell you that too.

Request a complimentary audit → Here

Sources:

ERCOT Adjusted Long-Term Load Forecast · ERCOT DAM HB_HOUSTON, HB_NORTH historical pricing

Commercial electricity use will likely surpass residential in 2027: EIA

TSP Large Load Interconnection Queue (2025)

GeoTel Data Center Inventory (2024).

ERCOT sourced RT/DA market data

TDL analysis reflects publicly available market data as of Q2 2026. This publication does not constitute financial, legal, or energy procurement advice.